All Categories

Featured

Table of Contents

Term Life Insurance Policy is a kind of life insurance plan that covers the insurance holder for a particular quantity of time, which is understood as the term. The term lengths vary according to what the private picks. Terms commonly range from 10 to three decades and increase in 5-year increments, offering level term insurance policy.

They typically give a quantity of coverage for a lot less than long-term kinds of life insurance policy. Like any kind of policy, term life insurance policy has benefits and drawbacks relying on what will work best for you. The advantages of term life include cost and the capability to customize your term length and insurance coverage quantity based on your needs.

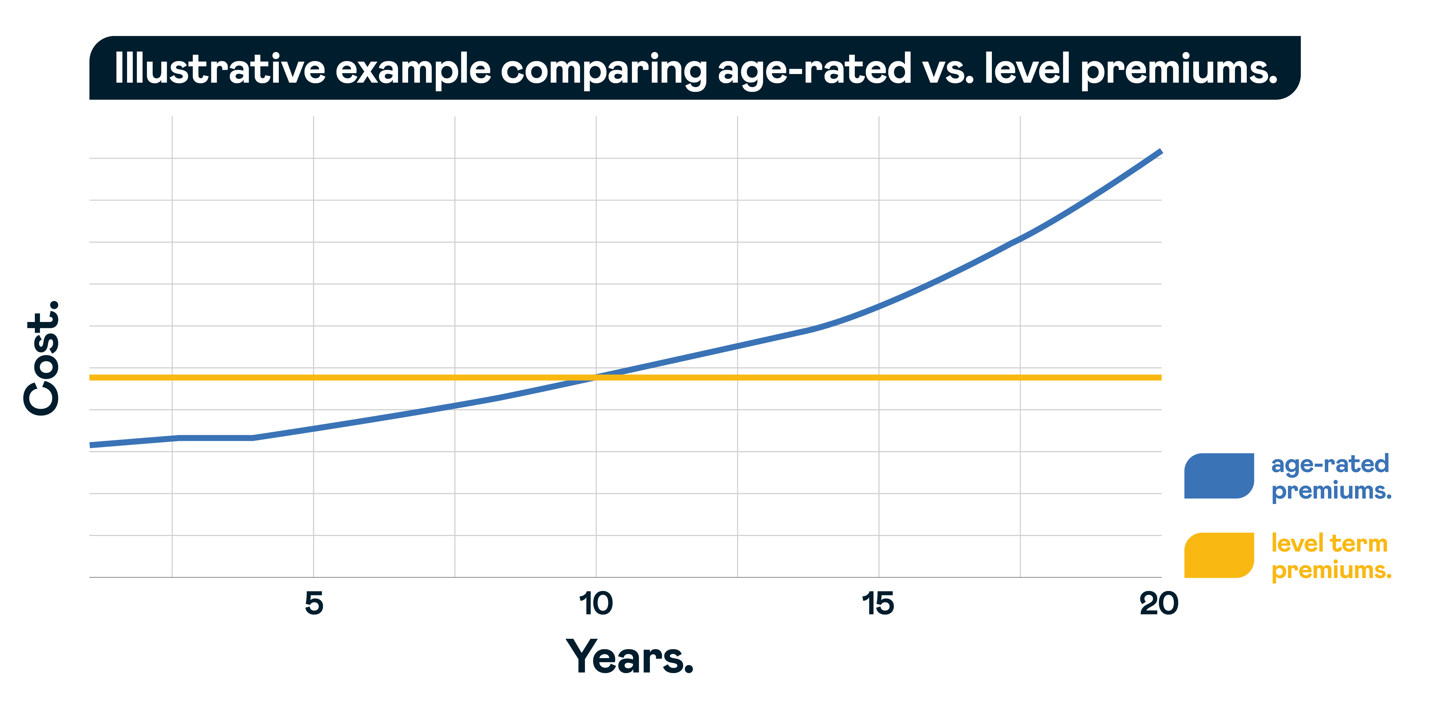

Depending on the kind of plan, term life can provide taken care of costs for the entire term or life insurance coverage on degree terms. The fatality benefits can be fixed.

You need to consult your tax advisors for your details accurate situation. *** Rates mirror policies in the Preferred And also Rate Class issues by American General 5 Stars My representative was really experienced and valuable in the process. No pressure to get and the process fasted. July 13, 2023 5 Stars I was pleased that all my requirements were fulfilled quickly and properly by all the representatives I talked to.

What is What Does Level Term Life Insurance Mean? Quick Overview

All paperwork was electronically completed with access to downloading for individual data upkeep. June 19, 2023 The endorsements/testimonials provided ought to not be taken as a recommendation to acquire, or a sign of the worth of any type of services or product. The endorsements are real Corebridge Direct clients that are not affiliated with Corebridge Direct and were not offered payment.

There are multiple types of term life insurance coverage policies. Instead of covering you for your entire life expectancy like entire life or global life policies, term life insurance policy only covers you for a designated amount of time. Plan terms normally range from 10 to 30 years, although shorter and much longer terms may be offered.

If you desire to maintain protection, a life insurer might supply you the alternative to restore the plan for another term. If you included a return of costs biker to your plan, you would certainly get some or all of the money you paid in costs if you have actually outlived your term.

Level term life insurance policy may be the best choice for those who want insurance coverage for a set time period and desire their costs to remain steady over the term. This may put on shoppers concerned about the price of life insurance and those who do not wish to alter their survivor benefit.

That is due to the fact that term policies are not assured to pay out, while permanent policies are, provided all premiums are paid., where the death benefit reduces over time.

On the other hand, you might be able to secure a less expensive life insurance policy rate if you open up the policy when you're younger. Similar to advanced age, bad health and wellness can additionally make you a riskier (and more expensive) prospect permanently insurance policy. If the condition is well-managed, you might still be able to locate budget friendly insurance coverage.

What is 30-year Level Term Life Insurance? The Key Points?

Health and age are usually a lot more impactful premium aspects than sex. High-risk hobbies, like scuba diving and skydiving, might lead you to pay more forever insurance. Risky jobs, like home window cleaning or tree cutting, may also drive up your price of life insurance. The ideal life insurance policy business and plan will rely on the individual looking, their individual score variables and what they need from their plan.

The first action is to establish what you require the plan for and what your budget is. Some business supply on-line quoting for life insurance policy, however numerous require you to call an agent over the phone or in individual.

1Term life insurance policy provides short-lived protection for an essential period of time and is usually more economical than irreversible life insurance coverage. 2Term conversion guidelines and constraints, such as timing, might use; for instance, there might be a ten-year conversion privilege for some products and a five-year conversion benefit for others.

3Rider Insured's Paid-Up Insurance coverage Acquisition Option in New York. 4Not offered in every state. There is a cost to exercise this motorcyclist. Products and cyclists are readily available in authorized jurisdictions and names and functions might vary. 5Dividends are not assured. Not all getting involved plan owners are eligible for returns. For pick cyclists, the problem relates to the guaranteed.

Our term life alternatives include 10, 15, 20, 25, 30, 35, and 40-year plans. One of the most preferred kind is level term, implying your payment (costs) and payout (survivor benefit) stays level, or the very same, up until completion of the term period. What is a level term life insurance policy. This is one of the most uncomplicated of life insurance policy options and requires extremely little maintenance for policy owners

You might offer 50% to your partner and split the remainder amongst your adult kids, a moms and dad, a friend, or even a charity. * In some circumstances the fatality advantage may not be tax-free, discover when life insurance policy is taxable.

What is Term Life Insurance Level Term? What You Need to Know?

There is no payment if the policy runs out prior to your death or you live beyond the policy term. You may have the ability to renew a term policy at expiration, yet the costs will certainly be recalculated based on your age at the time of renewal. Term life insurance policy is normally the least costly life insurance policy available because it provides a survivor benefit for a limited time and doesn't have a cash money value component like permanent insurance coverage - Term life insurance for spouse.

At age 50, the costs would rise to $67 a month. Term Life Insurance Rates thirty years old $18 $15 40 years old $28 $23 half a century old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life policy, for males and ladies in outstanding wellness. In comparison, below's a check out rates for a $100,000 entire life plan (which is a sort of permanent policy, implying it lasts your lifetime and includes money worth).

The lower threat is one aspect that enables insurers to bill reduced premiums. Rates of interest, the financials of the insurance provider, and state guidelines can also influence costs. As a whole, business typically use better rates at the "breakpoint" protection levels of $100,000, $250,000, $500,000, and $1,000,000. When you consider the quantity of coverage you can obtain for your costs bucks, term life insurance policy often tends to be the least costly life insurance policy.

{kind=link}

Latest Posts

Best Insurance To Cover Funeral Expenses

Final Expense Insurance Quotes Online

Burial Insurance Pro